- Consumer Products

- Energy & Natural Resources

- Education Sector

- Insurance Services

- Financial Services

- Healthcare Sector

- Manufacturing

- Not For Profit

- Public Sector

- Real Estate & Construction Sector

- Technology, Media & Telecommunications

- Travel, Tourism & Leisure

- Food and Restaurant

- Professional Services

-

Business Risk Service

Organisations must understand and manage risk and seek an appropriate balance between risk and opportunities.

-

Transaction Advisory, M& A, Business Consultancy

Transaction Advisory, M& A, Business Consultancy

-

IT Advisory

IT Advisory

-

Business Process Solutions

Business Process Solutions

-

Managing the VAT Audit

Managing the VAT Audit

-

Transfer Pricing

Global transfer pricing is all about understanding your business and the value drivers of your industry in an ever-changing environment.

Playing field or battlefield: what does the future look like for financial services?

16 Mar 2021Playing field or battlefield: what does the future look like for financial services?

2020 was the sort of year that few expected, and no one wanted. As we face a second year living with the effects of COVID-19, how do Financial Services companies view the immediate future and what plans do they have to move forward?

We surveyed 377 Financial Services business leaders, as part of our Global business pulse research[i], on their outlook for 2021, what they perceive as the oncoming challenges and how they are preparing for the future. Our research uncovered five key trends that resonated with industry leaders around the world. We asked a panel of our experts from London, New York and Singapore, to shed light on the market sentiment behind the figures and to give us their top tips for the year ahead.

- Going digital – there’s no time to waste

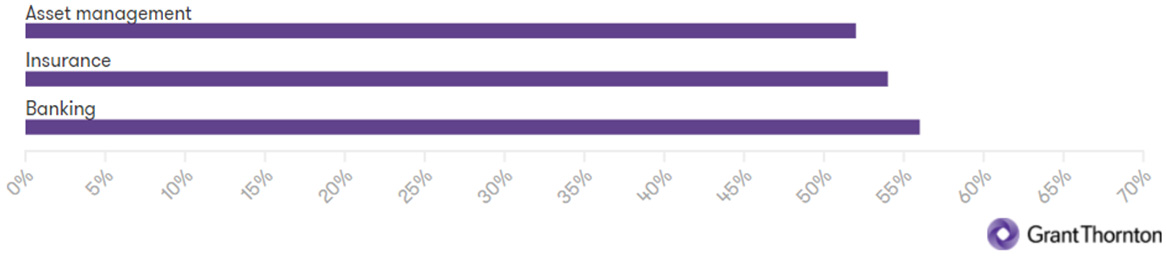

Our research showed, 56% of Banking, 54% of Insurance and 52% of Asset Management firms expect to increase their investment in IT over the coming year.

Percentage of businesses increasing investment in IT in the next 12 months

![]()

While digital transformation of Financial Services businesses is not new, it’s acceleration will be a key trend to watch in 2021.

“Digital has become a key focus,’ observes Sandy Kumar, Global Head of Financial Services and Business Risk Services and Partner at Grant Thornton UK. “There's been a compression in the time that clients are planning to implement transformation, the process is becoming more condensed. Investment in technology is a big area, along with the type of products that support it and people able to work with it to service clients in a more effective manner.”

The particular conditions created by the COVID-19 pandemic could also be speeding this trend, as Emily Lai, Business Risk Advisory Partner at Grant Thornton Singapore, has witnessed: “Companies are accelerating their pace on digitisation, shifting their business online, and moving quicker than before to improve efficiency. In the months ahead I think a lot of companies might need to redeploy and invest in technology to stay relevant.”

The process will be necessarily more challenging for larger, more established organisations, according to Matthew Cooleen, Risk Advisory Services Partner at Grant Thornton US. “Large Financial Services companies are going to need to evolve and it’s harder for them than the new start-ups – it's like an aircraft carrier turning versus a speedboat. They’re dealing with legacy systems from the 90s, so upgrading their systems and upgrading their working methodologies to a more agile environment will be critical.”

- A skills shortage threatens to frustrate growth

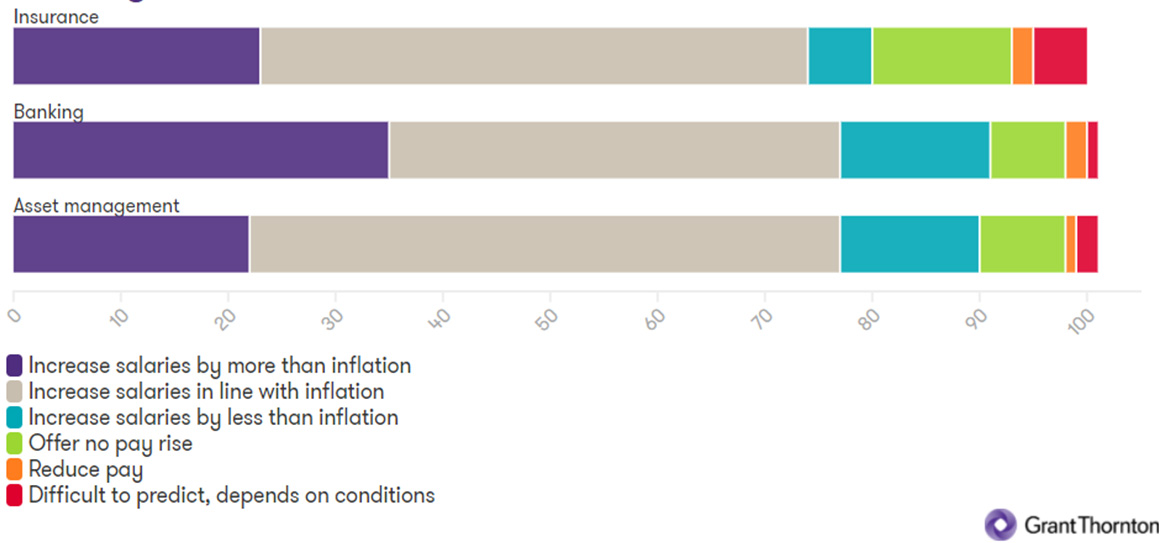

To compete and thrive in an increasingly digital marketplace, skilled labour is an essential requirement. Yet 65% of banking firms cited the availability of skilled workforce as a major constraint to growth, equally concerning as the current economic uncertainty. This unease also surfaced in the industry’s outlook on remuneration.

Industry outlook on remuneration![]()

The vast majority of Financial Services firms plan to increase salaries in 2021 in line with inflation, with 35% of banking firms predicting above inflation increases, compared to 21% of other industries, indicating that a shortage of talent could hold many companies back.

“Everybody's in competition now for the brightest and the best,” Matthew explains. “The FinTech’s showed the allure of hockey stick growth and fast wealth accumulation, which means banks are now competing with Fintech and private equity; they need to start showing that they can be competitive and are willing to fight for the best talent.”

Yet Emily believes it’s not just a question of paying for talent: “It's very hard to hire people with the right skillset at the moment – demand for tech talent is very high right now, but the supply is weak. Border restrictions and tighter foreign worker policies are only aggravating the talent shortage.”

For Sandy, both these issues resonate. “Clients are looking at mobility, focusing on other markets, to attract the talent they need in order to overcome barriers. But there’s also a definite sense of needing to reskill people to create a more agile workforce, particularly around technology, to ensure that the business is future fit.

“Even in our own business, we need to think about how we actually invest in our people and look at infrastructure refinement. Nobody is likely to be rushing back into the office, so having a clear strategy and policy to support people to work from home is vital, especially putting a bigger focus on people's wellbeing – looking after your people's health, their mindset, and how they are operating is key.”

-

We’re in this together: the new spirit of collaboration and innovation

Another area where the majority of Financial Services companies plan to invest more than other industries is Research and Development. With 52% of banking firms expected to increase spending in this area over the next year, it could indicate a need for new ways of working, new products, and new ways to grow. Across the board, our global team have all independently witnessed a growing tendency for business partnerships, collaboration and innovation; a positive takeout from the pandemic.

“Banks, asset management and insurance companies should leverage their allies and partnership opportunities to develop a fully digital ecosystem and get better access to technology innovation” says Emily. “In Singapore we are seeing banks collaborating with Fintech companies to offer e-commerce platforms. Even the traditional banks are going into crypto currencies and coming up with new ways of doing business to offer new solutions to their customers.”

Sandy sees a similar picture in the UK. “I think we will see some of the big retail banks align themselves much more closely with the big tech firms to improve their operations. They will have to do that rather than doing it all themselves, like Apple, Google and Amazon’s partnership around smart home tech.

“It’s a two-strand approach, offensive and defensive: defensive being how can you do the things you do more effectively, and offensive being how can you get to a bigger customer base in a more deliberate way, where people buy into your underlying product. To achieve both, I think partnerships will be important.”

Matthew agrees: “I think we’ll see collaboration between online retailers, social platforms and banks too. The one strength that the large financial institutions have is capital. And that's what the Fintech partners need. Because of that fact, I think we can expect to see many more Fintech partnerships and acquisitions. We’re seeing a new connectivity there that we hadn't seen before.”

-

Get ready for changes in customer behaviour

Another unifying trend across all three areas of Financial Services can be seen in their preparation for a recovery: all three sectors indicated they are already planning for changes to customer behaviour or competitive dynamics in varying degrees ( Asset Management 45%, Banking 28% and Insurance 36%). Our panel have all observed a new urgency of response to recent changes in customer behaviour during the pandemic.

Matthew explains: “During the pandemic we’ve seen a significant jump in mobile banking registrations contrasting with a big fall in branch transactions. This trend should permanently change the banks’ view on how to steer their consumer business going forward – companies need to implement what they've learned with COVID-19. I believe that this is a long-term fundamental shift in the ability to operate with agility, to speed up credit decisioning, and introduce new flexible working, workplaces and organisational strategies.”

“Things are becoming more competitive,” agrees Emily. “You may come up with new innovative ways to attract your customers, because there’s been a generation shift to the younger demographics, like millennials, who actually prefer digital channels. But businesses need to make the digital customer experience user-friendly for every audience, especially for the elderly. It needs to be more convenient, more personalised, easy and secure. Security is very important.”

“How you connect with clients is more important than ever,” Sandy concurs. “If you look at the vulnerable, the elderly, they may not be as acclimatised to digital. Suppliers need to consider if they are investing enough in educating their customer base and using platforms that will allow us to deal with those people and protect them against cybercrime and fraud.

“I also think that the gap between big and small business will narrow through new customer-led technology. Newer entrants who have leaner operating models may well be more successful, as long as they're able to convince customers that they have a solid, robust new product.”

-

Look on the bright side of life

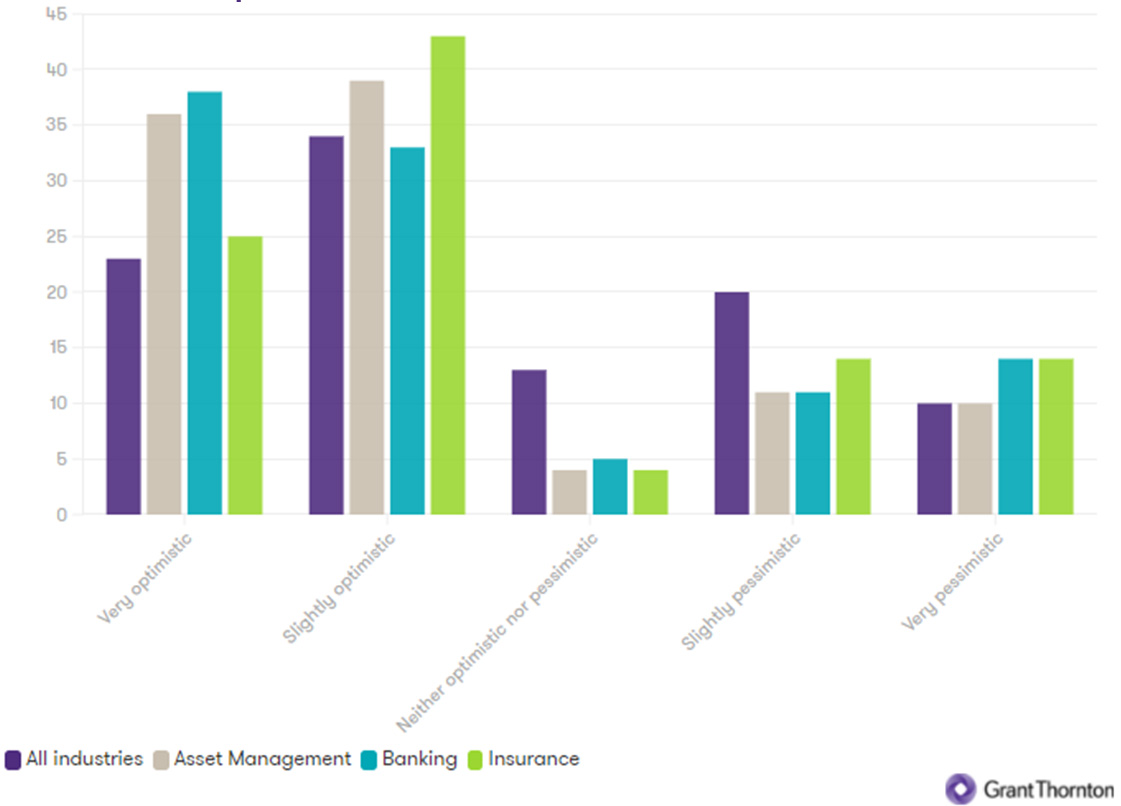

The research showed that over 40% of Financial Services businesses have grown revenue by more than 5% in the last 12 months, far more than the businesses who have lost a similar percentage of revenue. In addition, the majority are either optimistic or very optimistic about the economy in 2021 (in banking, this ranges from 63% in the EU to 73% across APAC and 74% in the Americas). But where does the optimism spring from and is it realistic?

Levels of economic optimism over the next 12 months

![]()

“I recognise the feeling of optimism,” says Sandy. “I think Financial Services is the vehicle through which governments execute their programmes, bringing liquidity to market. It’s fundamental to all of society – we save our money, we borrow from them, we trade through them – it creates a lot of movement and opportunity.

“Volatility in the market since March has meant that banks and organisations in the trading environment have seen a tremendously good year for themselves. We are likely to be entering a recession, and there will be a squeeze for the customer base which will mean less profit, but that doesn't mean no profit.

“I think it's a positive outlook, but COVID-19 still has a big impact on confidence. Until the pandemic subdues around the globe it continues to be the single biggest barrier to growth.”

“We’re emerging from an embattled position,” admits Matthew, “but 2020 was a good year for Financial Services in the US, and with renewed fiscal stimulus, the outlook is optimistic. Interest margins haven’t been impacted as much as one would think and the banks have adequate reserves to deploy and throw at emerging risks. In general, non-hospitality corporate entities have performed well through the pandemic and I do believe that there's general optimism that the vaccine is going to be impactful such that a mean reversion to normalcy should occur. At the heart of it all, I think the strength of the US infrastructure and economy is really showing itself.”

Emily sees the same possibilities in APAC: “Financial Services will be one of the key sectors driving the growth in Singapore and the economy is expected to rebound and grow. But it really depends on how well COVID-19 plays out with a vaccine now available, how effective it is and how the distribution works across all countries.”

We are currently working with Financial Services firms around the world to address the latest industry issues and achieve their strategic ambitions amidst the pandemic. For support navigating the year ahead, get in touch with local Grant Thornton Bahrain Financial Services adviser.

Jatin Karia

Senior Partnerjatin.karia@bh.gt.com

+973 39575562

Yaser Abbas SalmanPartner

yaser.abbas@bh.gt.com

+973 39402188